If you want to begin saving for your children’s college but are unsure where to start, this article will analyze different saving avenues and help you determine which one will be most effective for your situation. With the cost of higher education rising, it is advantageous to start saving as soon as possible.

According to Average Cost of College & Tuition by Hanson, “The average cost of attendance for a student living on campus at an in-state public four-year institution is $27,146 per year or $108,584 over four years. Out-of-state students pay $45,708 per year or $182,832 over four years. Private, nonprofit university students pay $58,628 annually or $234,512 over four years.” Below is a graph from the National Center for education statistics displaying how annual tuition costs from 1970-2023 have grown immensely.

Now that we have covered the cost and historical increases, let’s explore the different pathways to save for college. We’ll compare the Qualified Tuition Program (Section 529 Plan), Coverdell Education Savings Account (CESA), education savings bond program, and the use of student loans to cover the difference in lack of savings.

529 Plan

The Qualified Tuition Program, often called the 529 plan, is the most popular way to save. Anyone can use this because there is no phaseout limit for modified adjusted gross income. Another motivating factor behind the 529 plan is the wide range of expenses for which the funds are qualified. In general, you must use the money within the 529 for qualifying education expenses, often a combination of room/board, tuition, and books/supplies/equipment. The plan allows you to use the funds for all those, plus fees and equipment for certified apprentice programs. The investment benefit is that you will not have to pay tax on the 529 earnings when used for qualifying expenses.

The state sponsors these plans, and you can open an account in whichever state you prefer and use it for whatever school you prefer for undergraduate or graduate programs. Certain states offer tax deductions for contributions in an account. For example, if you live in Arizona, Arkansas, Kansas, Maine, Minnesota, Missouri, Montana, Ohio, or Pennsylvania, you can take a deduction on your taxes for your contribution (depending on the state, the 529 account might need to be sponsored in the state you reside in to get the tax deduction).

Distributions are excluded from gross income, and you can take the American Opportunity Tax Credit (AOTC) or Lifetime Learning Credit to reduce taxes (keeping in mind there are income phase-out limits for these tax credits). We’ll explore the tax credits in more depth below.

To avoid filing a gift tax form in 2024, if you are single, you can contribute up to $18,000 (gift amount) or front-load five years of gifting ($18,000*5=$90,000), which will double if you are married. This is the most lenient, popular, and tax-advantaged avenue to save for college. The 529 plan also allows you to use up to $10,000/year for qualified tuition expenses for grades K-12. Often, if a child attends a private school and pays tuition, this can be a reason to utilize the funds in your 529 plan.

Coverdell Education Savings Account

Next, we have the Coverdell Education Savings Account (CESA) which can be used for all undergraduate and graduate programs. The most significant limitation for this avenue is the income phaseout limit for singles in 2024, which is $95,000-$110,000, and for married filing jointly (MFJ), $190,000-$220,000. Some conditions are that you must withdraw the assets before age 30 unless the beneficiary has unique needs, and the contribution limit per beneficiary per year in 2024 is $2,000. If you have three children, you can only contribute $6,000 ($2,000 per child) in 2024. Some advantages are the same as those of a 529 plan: the leniency on what is considered a qualified expense and the fact that earnings are not taxed when used for qualified expenses.

Education Savings Bond

Now, the Education Savings Bond Program (Series EE and Series I). This avenue can give you capital for qualified educational expenses without incurring federal income tax on the interest earned, provided conditions are met. These bonds can be purchased at a low cost and grow over time. Like the CESA, there is a phaseout limit for income to determine who can use this avenue to save and must be redeemed by the bond owner or their dependent. In 2024, the phaseout for a single filer is $96,800-$111,800, and for married filing jointly (MFJ), $145,200-$175,200. You also may distribute up to the qualifying expenses you incur for the year.

Tax Credits

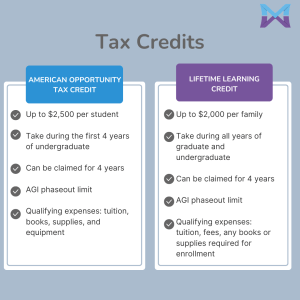

Let’s discuss the highlights of tax credits further. There is the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit that can reduce your tax liability (amount of taxes you owe). These can be used when paying for certain college expenses, not when contributing to a college savings fund. There are specific rules you must follow when applying for credit. These tax credits have a phaseout limit in 2024 of $80,000-$90,000 if you file single and $160,000-$180,000 if you’re MFJ. The AOTC has an annual credit limit of $2,500 per student, and qualified expenses include tuition payments, required enrollment fees, course materials, computers, and internet access. Only during the first four years of undergraduate expenses can you use the credit, and you must be enrolled at least half-time in a degree program.

On the other hand, Lifetime Learning Credit only allows you to take a credit of up to $2,000 per family per year. The credit can only be used for tuition and enrollment fees, which is less lenient than the AOTC. However, the credit can be applied (up to the limit) for all undergraduate and graduate-qualified expenses. These two credits can be taken simultaneously but can’t cover the same expenses. Because they are credits, they are applied directly to the amount of tax you owe to decrease it, and this is a great advantage to utilize.

A frequently asked question from clients is, what if I overfund the college savings account? This is why it is important only to fund the account for 80% of the expected costs because they are variable. If the beneficiary is finished with college expenses and there are still funds left over in the 529 account, to access that, you must pay a 10% penalty, and any earnings will be taxed at ordinary income for whoever takes the money out (owner or beneficiary) if used for non-qualified expenses. Thankfully, you also have the option to change the beneficiary on a 529 account to a close family member and use it for someone else’s education expenses. This can be helpful if you overfund the oldest child’s account and have younger children who need the money because you can just change the beneficiary and use it to pay for their qualified expenses.

Student Loans

If you discover you have underfunded expenses and need a loan, you have many options, such as a direct subsidized loan, an unsubsidized loan, a parent PLUS loan (government-funded), or a private loan ( privately funded).

Direct Subsidized Loan

A Direct Subsidized Loan is available to undergraduate students enrolled at least part-time and demonstrating financial need. You will need to begin repaying the loan, but interest only accrues after the grace period ends (six months after you finish school) or if you defer payments. During this grace period, the government covers the interest. This type of loan is often the best option to consider first. Your school determines the amount you can borrow and cannot exceed your estimated financial need.

Unsubsidized Loan

An unsubsidized loan is available to both undergraduate and graduate students without the requirement to demonstrate financial need. You are responsible for paying the interest at all times, even when you’re in school or payment is deferred. The maximum loan amount you can receive is limited to your school’s estimated financial need.

Parent Plus Loan

The Parent PLUS Loan is a federal loan program designed to help parents cover the cost of their child’s higher education. Unlike other federal student loans, the Parent PLUS Loan is taken out by the parents, not the student, and is intended to fill any gaps between the financial aid package and the total cost of attendance. Parents can borrow up to the total amount of the school’s estimated cost of attendance minus any other financial aid received. While the loan offers flexible repayment options and fixed interest rates, it’s essential for parents to be aware that they are responsible for the loan’s repayment and any accrued interest.

Private Student Loan

Private loans (from banks) typically have variable or fixed interest rates and may require a credit check and your creditworthiness, affecting the amount you can borrow. These loans often have fewer benefits than federal student loans, such as limited repayment options and lack of deferment flexibility.

Alternatively, borrowing from your 401(k) can provide access to funds without affecting your credit score, but it comes with risks like potential age penalties and tax implications. Additionally, tapping into your retirement savings can impact your long-term financial security, so you want to be sure and evaluate all your options.

Higher education savings avenues should be specific and catered to your financial situation. Hence, if unsure, talk to your financial advisor or schedule a free consultation with us. It is worthwhile to begin saving sooner rather than later, and this article will help you ponder your choices when saving for education expenses.